Guidelines & Procedures: Asset Acquisition

Asset Purchases

All asset purchases made on behalf of Rice University must be made in accordance with the Rice University Purchasing Policy (available here: Policy No. 814: Rice University Purchasing Policy).

Asset purchases involving contracts must be made in accordance with the Rice University Policy on Signature and Approval Authority for Contracts available here: Policy 810: Signature and Approval Authority for Contracts).

If your purchase requires a certificate of insurance, additional information is available here: Certificates of Insurance

The Rice University Purchasing & Payment Policy (available here: Purchasing & Payment Policy) provides detailed guidelines and instructions regarding the tasks required to maintain compliance.

Acquisition Reporting and Tagging

Once the initial invoice for an asset purchase has been paid, a property tag is created and affixed to the equipment/property.

Asset Tags allow the Rice University property to be correctly identified by the responsible department members, Property Accounting, and internal/external auditors. Work with Property Accounting to affix an asset tag to the corresponding asset upon receipt.

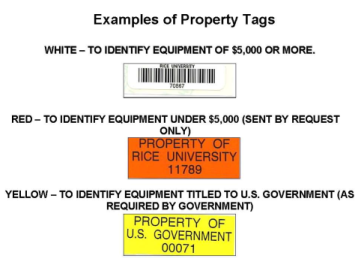

Rice uses three kinds of equipment and property ID tags. Property Accounting furnishes all tags:

- A white ID tag identifies equipment with a cost of $5,000 or more, which is capitalized as an asset and subject to the biennial inventory.

- A red ID tag identifies property with a cost of less than $5,000. Red tags are only provided to departments upon request to assist with property control and to help identify items not subject to the biennial inventory. Property Accounting does not track the issuance of these tags as they are for administrative purposes only.

- A YELLOW ID TAG identifies equipment titled to the U.S. government. This includes equipment loaned to the University by a government agency or equipment purchased by the University using research funds whose award documents state that all the title to all purchased equipment vest with the government.

Samples of the three types of tags currently in use are shown below:

Note: Certain equipment cannot be tagged, such as such as lasers, software, and heat sensitive items, but must still be inventoried. In such cases, the item will be assigned an equipment number (PTag) but will not be tagged. It is the department’s responsibility to notify Property Accounting whether or not an item may be tagged. A white ID tag will be assigned to the equipment and mailed to the department to be kept on file. It must be presented during the biennial equipment inventory. The equipment number in FAS for the non-taggable item will have the suffix ‘NT’ added, e.g., 12345NT, as an indication the equipment is non-taggable.

Fabrication

Occasionally, a piece of equipment that is needed to conduct research is not available for purchase from a vendor. Fabrication is the process of creating a unique fabricated item to meet a specific research requirement. The fabricated item is assembled from a number of parts, supplies and components, and as such is comprised of individual items which cannot function or be useful alone, or which lose their individual identity when incorporated into the fabricated item.

If the fabricated item is expected to have a combined cost of $5,000 or more and a useful life of more than one year. The following steps are required:

- Please be sure to indicate the Fund-Org-Acct of the funding sources of the item.

- The completed and signed form may be emailed to fascard@rice.edu.

Property Accounting, Research & Cost Accounting, and the Office of Sponsored Research (if necessary) will review the request for a Fabrication Fund to determine whether the work contemplated is in accordance with the terms and conditions of the funding sources.

- If approved, Research & Cost Accounting will establish a new Fabrication project number (or issue a new sub-project number if the fabrication is part of an existing project), process the budget revision to transfer the funds to the new fund or sub-fund, and inform you of the fund or sub-fund number. This new Fabrication project number will be used to identify all costs relating to the fabricated item, and a capital account code is to be used for all charges. The expenditure type EQP:FabricationEquipment must be used for all costs associated with the Fabrication.

- If denied, Research & Cost Accounting will explain the issues that need to be addressed. Your request may be denied if the planned fabrication violates the terms and conditions of any of the funding sources.

Each purchase of a component for a fabricated item must be made in accordance with the Rice University Purchasing Policy.

Equipment Transfer

For the purposes of property and equipment control, the term “Transfer” can apply to:

- Change in the Rice University organization that is responsible for the item “Interdepartmental Transfer”

- Change in the title or ownership of items (A) coming to Rice from another organization with a new faculty member“Incoming Professor” or (B) leaving Rice to another organization with an exiting faculty member“Exiting Professor”

Interdepartmental Transfer or Sale

An asset that is no longer of use to a department should usually be disposed in accordance with the Disposal Procedures defined elsewhere in this document. In some cases, before the item is listed in the Rice Classifieds, another department is identified that wishes to use the equipment. Responsibility for the property may be transferred to the new department at no cost or sold to that department at an agreed upon price.

- If an asset is to be transferred:

- The department relinquishing control of the property must (1) notify Property Accounting by email or memo, and (2) if receiving payment from the new department, initiate an Interdepartmental Transfer (IDT) to transfer payment, instructions here: Internal Transfer, see Interdepartmental Transfer (IDT).

- The department accepting control of the property should submit an equipment transfer via the Disposal form to Property Accounting.

- Property Accounting reviews the documentation submitted and approves the Disposal form

Transfer of Equipment - Incoming Professor -See also Policy 331

To transfer equipment from their previous university, an incoming faculty member should submit the following documentation to Property Accounting (fascard@rice.edu)

- Completed Transferred Property Form

- Completed Property Control Registration Form for each piece of equipment.

- Copy of the approval(s) to transfer equipment from the previous institution.

- Documentation of original acquisition date and cost of each piece of equipment.If documentation of the original purchasing information is not available, this information must be provided on the Transferred Property Form based on the transferring institution’s records. In this case, Property Accounting or another authorized official of the transferring institution must sign the form.

- If the transferred equipment is part of a fabrication that is new to Rice, complete a Fabrication Form. If the transferred equipment is part of an existing fabrication, provide the fund number.

- If any Rice Purchase Orders or invoices payable to Rice have been created or paid in association with this transfer, provide a copy of each.

- If the previous institution is receiving payment as a condition of this transfer, provide a written description or copy of the agreement and the current status of payments.

Transfer of Equipment - Exiting Professor

When transfers occur because a professor is leaving Rice and wishes to transfer the title of Rice-owned equipment, the following actions are required:

- The Department Chair or Dean must provide a memorandum to the Vice President of Finance (VPF) stating that the transfer is appropriate, the reason(s) why it is appropriate, that the equipment is not required at Rice for other research and that any expected payment is fair to Rice University. This memorandum must be accompanied by an invoice and bill of sale for the equipment and a Transfer of Title for Exiting Professors Form (PDF) listing the equipment to be transferred.

- A copy of the memorandum, invoice, bill of sale and form must be submitted to Property Accounting for review.

- Property Accounting will review the documents to ensure that Rice holds clear title to the equipment and that the expected payment amount is reasonable in relation to the net depreciated value of the asset(s). Property Accounting will inform the VPF and department of the results of that review. If Rice does not hold clear title to any of the items in question, Property Accounting will work with Research and Cost Accounting, the Office of Sponsored Research and the department to attempt to resolve the issues and obtain clear title. If title cannot be obtained, the department will be informed that the item(s) may not be transferred. Title to equipment may not be transferred until all issues are resolved.

- Once the VPF approves, all original documents with appropriate signature, are returned to the originating office, and copies are sent to Property Accounting.

- After receiving the signed documents, the originating official is responsible for sending the invoice for payment and coordinating the removal of the equipment from Rice.

- For items purchased using grant funds, the proceeds of the sale must be deposited into the grant(s) used to purchase the equipment, if still open. For items purchased using University funds, the organization that provided the funds designates where the proceeds are deposited.

Donations

Acquisition of equipment or property through donations must be made in accordance with Resource Development’s “Gift Policy and Procedure Document” Section III.B.5, Tangible personal property. For a copy of this document, contact Resource Development at 713-348-4600 or giving@rice.edu.

Lease

Property may be acquired by lease rather than purchase. For additional information, see Section 4.E, Lease vs. Purchase Decision Making of the Rice University Purchasing & Payment Policy (available here:Purchasing & Payment Policy). Property acquired by entering into a “Capital Lease” will be subject to the same control and reporting requirements as property that is purchased.